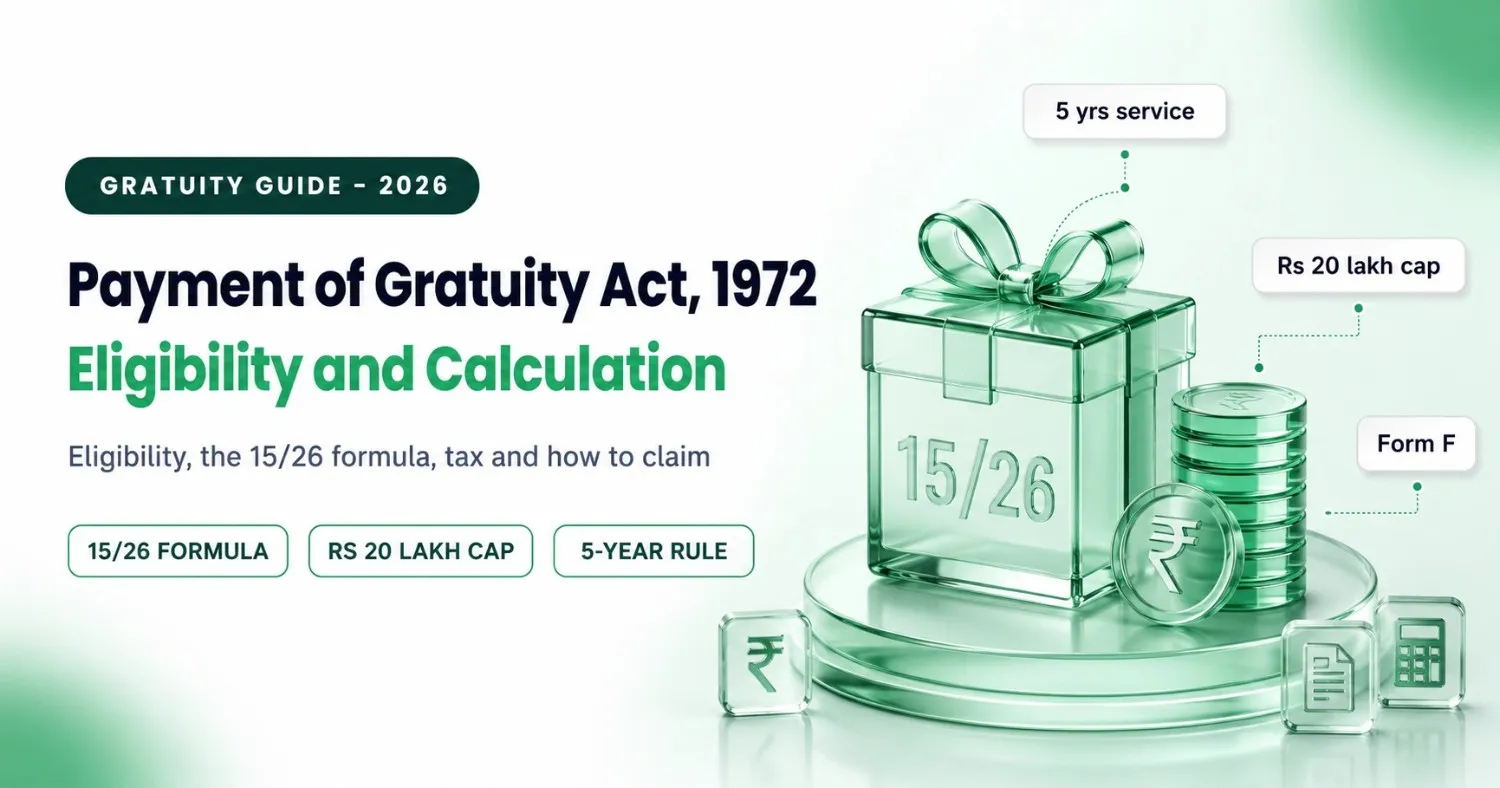

Gratuity is a lump sum your employer pays you for long service, and you become eligible after five years of continuous service. It is a legal right, not a bonus or a favour. The rules sit in the Payment of Gratuity Act, 1972. This guide explains who qualifies, how the amount is worked out, how it is taxed, and how to claim it without a dispute.

- Gratuity is payable after 5 years of continuous service. Death or disablement waives the 5 year rule.

- The Act applies to establishments with 10 or more employees, and once it applies, it keeps applying.

- The formula is (15 / 26) x last drawn basic plus DA x completed years. Service beyond 6 months rounds up to a full year.

- The protected ceiling is Rs 20 lakh. The formula amount is tax free for covered employees, and government employees pay no tax.

- Gratuity can be forfeited only under Section 4(6), for damage to employer property, violence or moral turpitude, and only with due process.

- The employer must pay within 30 days or owe simple interest. Disputes go to the Controlling Authority.

What is gratuity under the Payment of Gratuity Act, 1972

Gratuity is a one-time payment from an employer to an employee for continuous service. The Payment of Gratuity Act, 1972 makes it a statutory right in India. It is paid when you leave, on retirement, resignation, death or disablement.

Think of it as a thank you for staying, but one the law makes compulsory. Your employer cannot treat it as optional once you meet the conditions below.

Who is eligible for gratuity

You are eligible for gratuity once you complete five years of continuous service with the same employer. This rule sits in Section 4 of the Act. Continuous service is defined in Section 2A.

There is one important exception. The five year condition is waived if your service ends due to death or disablement. In those cases gratuity is payable even if you served less than five years.

One nuance saves many people who think they are short. Under Section 2A, 240 days of work in a year counts as a full year. Courts have read this to mean that 4 years and 240 days in the fifth year can make you eligible. So count your exact days before you assume you do not qualify.

Which establishments the Act covers

The Act applies to factories, mines, oilfields, plantations, ports, railways and shops or establishments with 10 or more employees on any day in the preceding 12 months. This threshold is set in Section 1(3).

Once the Act applies to an establishment, it continues to apply even if the headcount later drops below 10. So a growing business stays covered for good once it crosses the line.

How to calculate gratuity

For employees covered by the Act, the formula is fixed:

Gratuity = (15 / 26) x last drawn monthly wages x completed years of service

Here "wages" means basic salary plus dearness allowance. The figure 26 is the assumed number of working days in a month, and 15 stands for 15 days of wages for each completed year. Any service beyond six months in the final year is rounded up to a full year.

A worked example. If your last drawn basic plus DA is Rs 50,000 and you served 8 years and 7 months, the service rounds up to 9 years.

Gratuity = (15 / 26) x 50,000 x 9 = Rs 2,59,615.

The table below shows how the amount grows with tenure on a Rs 50,000 last drawn wage.

| Last drawn wages (basic + DA) | Completed years | Gratuity payable |

|---|---|---|

| Rs 50,000 | 5 years | Rs 1,44,231 |

| Rs 50,000 | 10 years | Rs 2,88,462 |

| Rs 50,000 | 15 years | Rs 4,32,692 |

| Rs 50,000 | 20 years | Rs 5,76,923 |

To get the exact figure for any salary and tenure in seconds, use the gratuity calculator instead of building a spreadsheet. Since gratuity sits inside your wage structure, it also helps to view it against your full salary structure.

The Rs 20 lakh ceiling and how gratuity is taxed

There is a cap on the gratuity protected by law. The statutory ceiling is Rs 20,00,000, raised from Rs 10 lakh by the 2018 amendment. Your employer can pay more, but anything above the formula is treated differently for tax.

How gratuity is taxed depends on who you are. The rules sit in Section 10(10) of the Income Tax Act, 1961.

- Government employees: gratuity is fully exempt from tax.

- Employees covered by the Act: exempt up to the least of the actual gratuity received, Rs 20 lakh, or the formula amount.

So for most private sector employees the formula amount is tax free, and only the excess is taxed. To see how a payout changes your in-hand figure, check it against your take-home salary.

When gratuity can be forfeited

Gratuity is not automatically lost when you are dismissed. It can be forfeited only in specific cases set out in Section 4(6), and only when your service is terminated for those reasons.

- If your service is terminated for an act, wilful omission or negligence that causes damage or loss to the employer's property, gratuity can be forfeited to the extent of that loss.

- If your service is terminated for riotous or disorderly conduct, an act of violence, or an offence involving moral turpitude committed in the course of employment, gratuity can be forfeited wholly or partly.

Forfeiture needs a proven reason and proper procedure. An employer cannot simply withhold gratuity because they were unhappy with you. The employee must get a chance to be heard before any amount is forfeited.

Nomination: protect your family

Section 6 requires you to file a nomination. You do this in Form F, within 30 days of completing one year of service. The nominee receives your gratuity if you die.

If you have a family, the nomination must be in favour of a family member. A nomination in favour of someone outside your family is void. If you marry later, file a fresh nomination in Form G. Keeping this current avoids your family fighting for the amount as legal heirs.

How to claim gratuity and the payment timeline

The process is straightforward when both sides follow it.

- You apply to the employer in writing, usually in Form I, within 30 days of gratuity becoming payable.

- The employer must calculate the amount and pay it within 30 days of it becoming due, under Section 7.

- If the employer pays late, they owe simple interest for the delay period.

If there is a dispute, it goes to the Controlling Authority appointed under the Act. You can appeal the order to the Appellate Authority. So a refusal to pay is not the end of the road. The law gives you a clear forum.

Compulsory insurance for employers

Section 4A requires most employers to insure their gratuity liability. This is usually done through a Life Insurance Corporation group scheme or another approved insurer, unless the employer runs an established and registered gratuity fund. Central and state government employers are exempt. This protects employees even if a company runs into financial trouble.

Penalties for non-compliance

The Act has teeth. Section 9 sets out the penalties.

- A false statement to avoid payment can attract imprisonment up to 6 months, a fine up to Rs 10,000, or both.

- A general contravention of the Act can attract imprisonment from 3 months to 1 year, or a fine of Rs 10,000 up to Rs 20,000.

- Failure to pay gratuity that is due can attract imprisonment from 6 months up to 2 years.

Gratuity and the new labour codes

The Code on Social Security, 2020 carries gratuity forward and adds one big change. Fixed term employees become eligible for gratuity on a pro-rata basis, without waiting for five years. So a worker on a one year fixed term contract can earn gratuity for that year. For the wider picture, see our guide to Indian labour laws.

How employers stay compliant

Gratuity rarely fails because the rules are hard. It fails because the records are not ready on exit. The fix is to track continuous service, basic plus DA and nominations from day one, and to settle gratuity inside the full and final process along with leave encashment and dues.

Gratuity is one of three statutory payouts most Indian employees should understand together. The other two are covered in our guides to the EPF Act, 1952 and the Payment of Bonus Act, 1965. Modern payroll systems such as factoHR India compute all three on the correct wages and run a one click full and final settlement, so nobody relies on memory at exit.

Quick Recap

| Rule | Position under the Act |

|---|---|

| Applies to | Establishments with 10+ employees (Section 1(3)) |

| Eligibility | 5 years continuous service; waived on death or disablement (Section 4) |

| Formula | (15 / 26) x last drawn basic + DA x completed years |

| Ceiling | Rs 20,00,000 (2018 amendment) |

| Tax | Govt employees fully exempt; others exempt up to least of amount, Rs 20 lakh, or formula (Section 10(10)) |

| Forfeiture | Only under Section 4(6), with due process |

| Nomination | Form F, within 30 days of completing 1 year (Section 6) |

| Payment | Within 30 days, simple interest if late (Section 7) |

| Now governed by | Code on Social Security, 2020 (fixed-term employees get pro-rata) |

Frequently asked questions

Is gratuity paid before 5 years of service?

No, not in the normal case. You need five years of continuous service under Section 4. The only exceptions are death or disablement, where the five year rule is waived. Also count your exact days, since 4 years and 240 days in the fifth year can make you eligible.

How is gratuity calculated for private employees?

For employees covered by the Act, gratuity is (15 / 26) x last drawn monthly basic plus DA x completed years of service. Service beyond six months in the final year rounds up to a full year. The protected ceiling is Rs 20 lakh.

Is gratuity taxable in India?

Government employees pay no tax on gratuity. For employees covered by the Act, gratuity is exempt up to the least of the amount received, Rs 20 lakh, or the formula figure. Only any excess above that is taxed.

Can an employer refuse to pay gratuity?

Only in the narrow cases under Section 4(6), such as termination for damage to the employer's property, violence or moral turpitude, and only after due process. An employer cannot withhold gratuity simply because of a dismissal. You can approach the Controlling Authority if it is wrongly denied.

What is the time limit for an employer to pay gratuity?

The employer must pay gratuity within 30 days of it becoming due, under Section 7. If they pay late, they owe simple interest for the delay. You apply in Form I, usually within 30 days of the amount becoming payable.

Do fixed term employees get gratuity?

Yes, under the Code on Social Security, 2020 a fixed term employee earns gratuity on a pro-rata basis, without the five year condition. This is a major change from the older position that required five continuous years.