The EPF Act 1952 makes provident fund a legal right for most salaried employees in India, not an optional perk. If your establishment qualifies, you must deduct and deposit provident fund every month, and the contribution earns guaranteed interest set by the government each year.

This guide explains who the Act covers, who must be enrolled, how the 12 percent contribution is split, the current interest rate, the tax rules, and a major 2026 update on the wage ceiling.

- The Act applies to every factory and establishment with 20 or more employees, and once it applies, it keeps applying.

- Employees earning basic plus DA up to Rs 15,000 a month must be enrolled. Those earning more can join with employer consent.

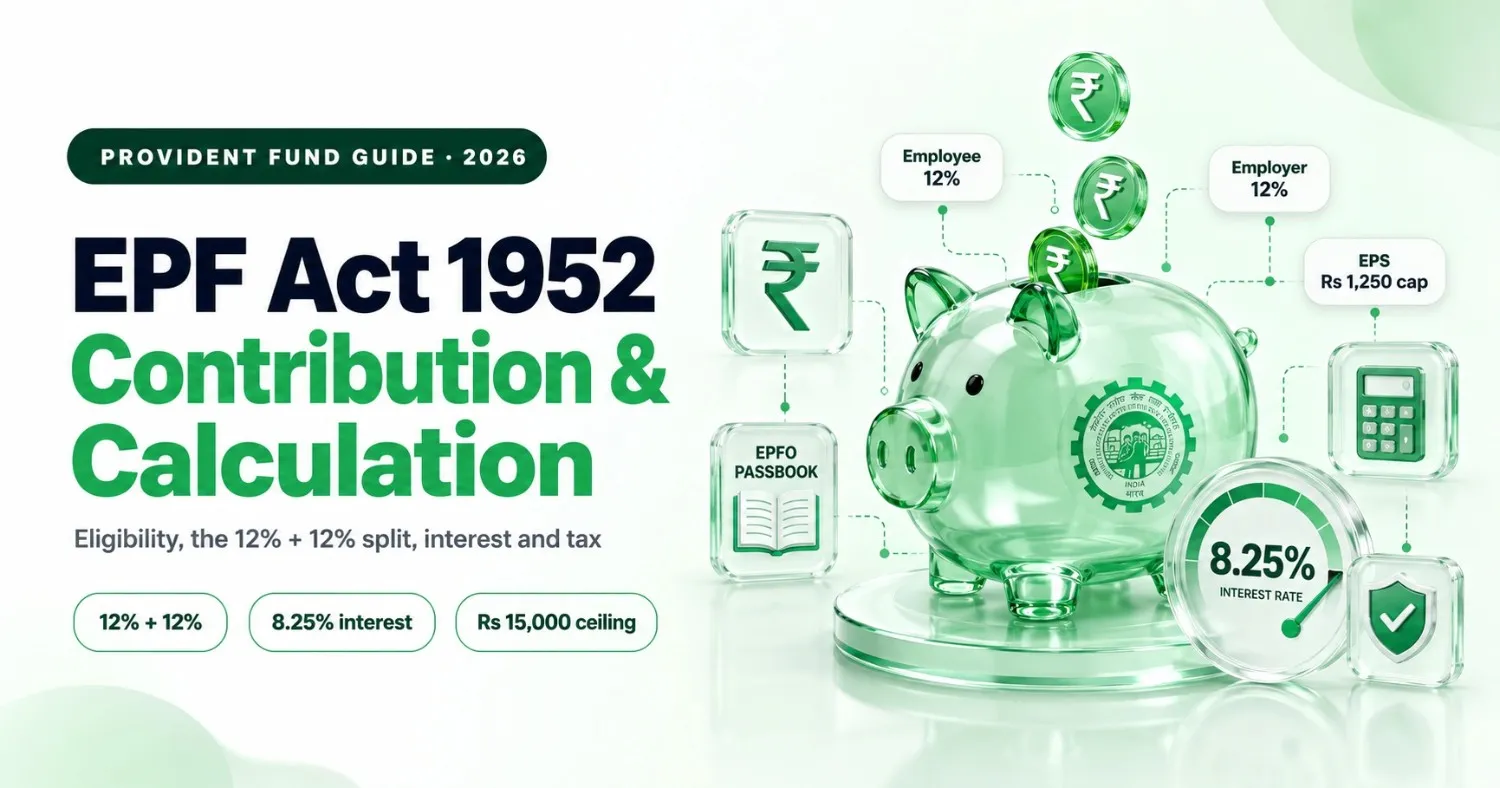

- The employee contributes 12 percent and the employer contributes 12 percent of basic plus DA.

- The employer's 12 percent splits into 8.33 percent to the pension scheme (capped at Rs 1,250) and 3.67 percent to EPF.

- The EPF interest rate for FY 2025-26 is 8.25 percent, credited once a year.

- EPF is tax-free if you withdraw after 5 years of continuous service. The wage ceiling of Rs 15,000 may soon rise.

What is the EPF Act 1952?

The EPF Act 1952, formally the Employees' Provident Funds and Miscellaneous Provisions Act, 1952, is the law that builds a retirement corpus for salaried workers in India. It is run by the Employees' Provident Fund Organisation, or EPFO.

The Act runs three schemes together: the Employees' Provident Fund (savings), the Employees' Pension Scheme 1995 (pension), and the Employees' Deposit Linked Insurance scheme (life cover). Your monthly contribution feeds all three.

Which Establishments Must Register?

EPF coverage is triggered by headcount:

- Every factory in a scheduled industry, and every other establishment, that employs 20 or more persons.

- Once the Act applies, it continues to apply even if your headcount later drops below 20.

An establishment with fewer than 20 employees can also join voluntarily under Section 1(4), with the consent of the employer and employees. Registration is due within 15 days of crossing the threshold.

Who Must Be Enrolled?

Enrolment depends on wages, counted as basic plus dearness allowance:

- An employee earning up to Rs 15,000 a month must be enrolled in EPF. This is the statutory wage ceiling.

- An employee earning above Rs 15,000 is an "excluded employee" and can stay out, but most join with employer consent.

- An employee who is already an EPF member continues in the scheme even after crossing Rs 15,000.

Every member gets a Universal Account Number (UAN) that stays the same across jobs, and files Form 11 to declare prior membership.

How Much Is Contributed? The 12 Percent Split

Both sides contribute 12 percent of basic plus DA, but they flow differently:

- Employee: the full 12 percent goes into the EPF account.

- Employer: 12 percent is split. 8.33 percent goes to the Employees' Pension Scheme, capped at Rs 1,250 a month on the Rs 15,000 ceiling. The balance, 3.67 percent, goes into EPF.

- The employer also pays a small EDLI charge of 0.5 percent for life cover, plus EPF administration charges.

How to Calculate EPF (Worked Example)

Take an employee with basic plus DA of Rs 15,000 a month.

- Employee contribution: 12 percent of Rs 15,000 = Rs 1,800, all into EPF.

- Employer to pension (EPS): 8.33 percent of Rs 15,000 = Rs 1,250.

- Employer to EPF: 3.67 percent of Rs 15,000 = Rs 550.

- Total going into the fund each month: Rs 1,800 plus Rs 550 plus Rs 1,250 = Rs 3,600.

To work out the exact figures for any salary, including the pension cap, use the EPF calculator instead of doing it by hand. It also helps to view PF alongside your full salary structure, since PF sits inside your CTC.

What Is the EPF Interest Rate?

The government sets the EPF interest rate every year. For FY 2025-26 it is 8.25 percent per annum. Interest is calculated on the monthly running balance but credited to your account once a year, at the end of the financial year.

This guaranteed, compounding return is what makes EPF one of the safest long-term savings tools for Indian employees.

Is EPF Taxable?

EPF enjoys an exempt-exempt-exempt status, so contributions, interest, and maturity are normally tax-free. Two limits apply:

- Interest on your own contributions above Rs 2.5 lakh in a year is taxable.

- If you withdraw before completing 5 years of continuous service, the amount becomes taxable and TDS may apply.

Withdraw after 5 years and the entire amount, including interest, is tax-free. Gratuity rewards the same long service; see our guide to the Payment of Gratuity Act, 1972. To see how PF affects your monthly figure, check your take-home salary.

Withdrawal, Transfer, and VPF

When you change jobs, transfer your EPF using the same UAN rather than withdrawing, so your service stays continuous and tax-free. Full withdrawal is allowed at retirement or after two months of unemployment. Partial withdrawals are allowed for housing, medical needs, marriage, and education.

If you want to save more, the Voluntary Provident Fund lets you contribute beyond the mandatory 12 percent, earning the same interest rate. The employer is not required to match the extra amount.

The Wage Ceiling Update You Should Track

The EPF wage ceiling has stayed at Rs 15,000 since 2014. That is set to change. As of January 2026, the Supreme Court directed the central government and EPFO to take a final decision on raising the ceiling, with figures of Rs 21,000 and Rs 25,000 under discussion.

If the ceiling rises, both employee and employer contributions go up for anyone earning above Rs 15,000, which increases retirement savings but also raises monthly deductions and employer cost. Watch for the official notification before you revise payroll.

How the Code on Social Security 2020 Changes This

The EPF Act 1952 is now subsumed under the Code on Social Security, 2020, one of the four labour codes notified effective 21 November 2025 with rollout from 1 April 2026. The provident fund framework continues, but two things matter:

- The new definition of wages caps allowances, so basic wages must be at least 50 percent of total pay. This 50 percent rule lifts the base used for PF, which raises both your savings and employer cost.

- Social security coverage is being extended, including to gig and platform workers.

Central and state rules are still being finalised, so confirm the current position for your establishment. For the wider view, see the India labour codes guide.

Quick Recap

| Rule | Position under the Act |

|---|---|

| Applies to | Factories and establishments with 20+ employees |

| Wage ceiling | Rs 15,000 a month (basic + DA), revision under Supreme Court direction |

| Employee contribution | 12 percent of basic + DA |

| Employer contribution | 12 percent (8.33% to EPS capped at Rs 1,250, 3.67% to EPF) |

| Interest rate | 8.25 percent for FY 2025-26, credited yearly |

| Taxability | Tax-free after 5 years of continuous service |

| Account | One UAN across all jobs |

| Now governed by | Code on Social Security, 2020 |

Frequently Asked Questions

Is EPF deduction mandatory if my salary is above Rs 21,000?

The statutory wage ceiling is Rs 15,000, not Rs 21,000. If you earn above Rs 15,000 and were never an EPF member, you can opt out. But if you are already a member, deduction continues regardless of salary.

What is the EPF contribution percentage?

The employee contributes 12 percent of basic plus DA, and the employer contributes another 12 percent. The employer's share splits into 8.33 percent to the pension scheme, capped at Rs 1,250, and 3.67 percent to EPF.

What is the current EPF interest rate?

For the financial year 2025-26 the rate is 8.25 percent per annum. It is calculated monthly on the running balance and credited to your account once a year.

When can I withdraw EPF without tax?

Withdraw after 5 years of continuous service and the full amount, including interest, is tax-free with no TDS. Withdraw earlier and it becomes taxable.

Can a company with fewer than 20 employees register for EPF?

Yes. Under Section 1(4), a smaller establishment can join voluntarily with the consent of the employer and the employees, with no minimum headcount.

What is the difference between EPF and EPS?

EPF is your savings fund that you can withdraw. EPS is the pension scheme funded by 8.33 percent of the employer's share, capped at Rs 1,250 a month, which pays a monthly pension after retirement.

Will the EPF wage ceiling increase in 2026?

It may. The ceiling has been Rs 15,000 since 2014, but in January 2026 the Supreme Court directed the central government and EPFO to decide on raising it, with Rs 21,000 and Rs 25,000 under discussion. Nothing is final until an official notification, so keep payroll on Rs 15,000 until then.

Is EPF now governed by the Code on Social Security 2020?

Yes. The EPF Act 1952 has been subsumed under the Code on Social Security, 2020, which took effect from 21 November 2025 with rollout from 1 April 2026. The provident fund rules continue, but they now sit inside the new code, and central and state rules are still being finalised.

Does the new 50 percent wages rule increase my PF?

For many employees, yes. Under the labour codes, basic wages must be at least 50 percent of total pay. If your basic was lower, the higher basic raises the base for the 12 percent PF contribution, so both your PF savings and your employer's cost go up.

Make EPF Compliance Effortless

EPF looks simple until you handle the pension cap, EDLI and admin charges, UAN management, and monthly ECR filing across locations. factoHR India applies the correct split automatically, files the monthly challan, manages UAN and KYC, and keeps your provident fund records audit-ready. So payroll closes on time, every month.